The month of August, typically slow in the property market, was even slower this year due to concerns around inflation and rising interest rates. But according to the latest data from the Real Estate Institute of New Zealand (REINZ), there were also early signs of a Spring ‘warm up’.

For more on this, here’s what’s happening in the housing market.

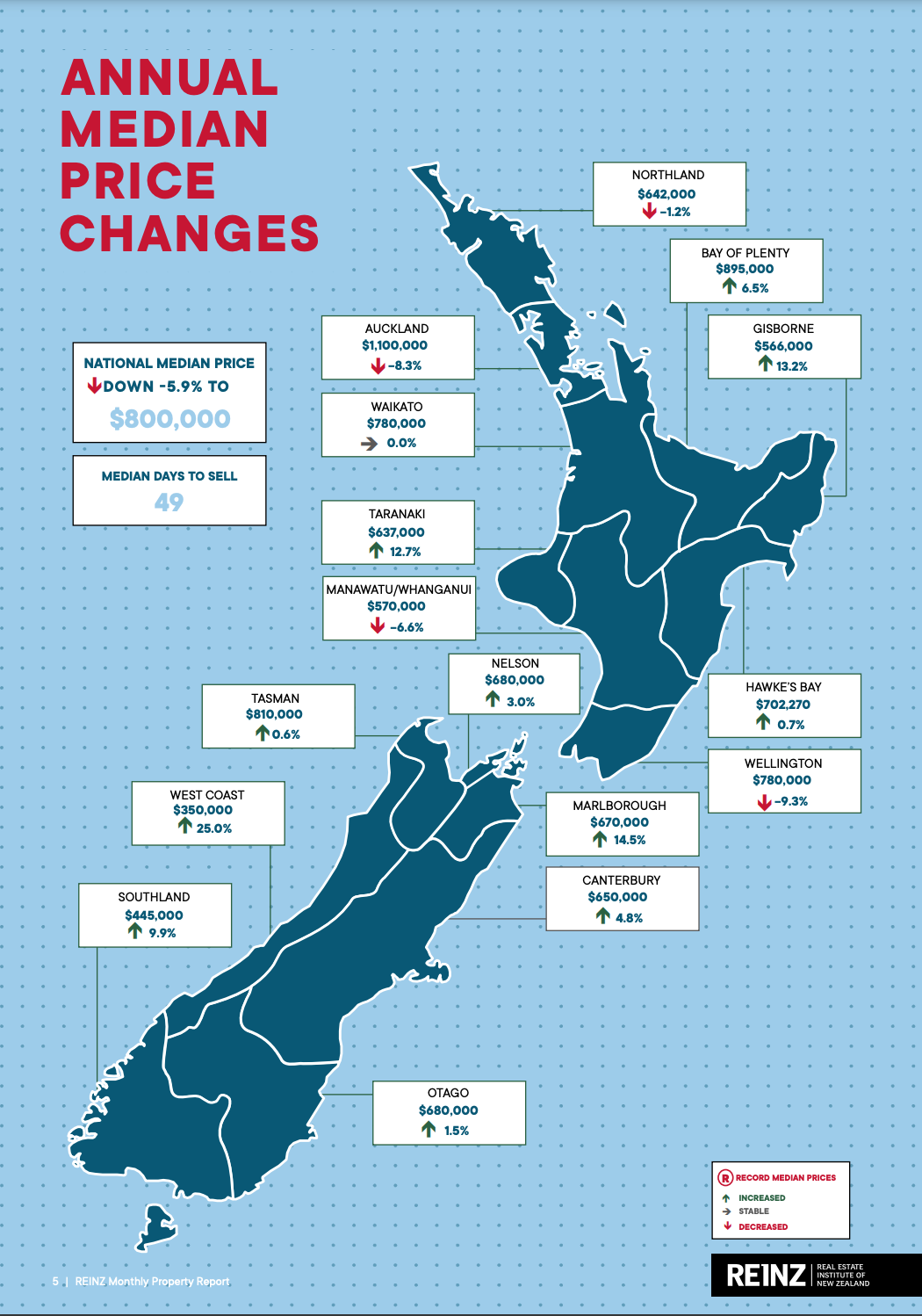

Auckland and Wellington drive national median price down

In August 2022, the median property price across New Zealand dropped 5.9% year-on-year, from $850,000 to $800,000. It was also a 1.2% decrease compared to July 2022.

Amongst the four regions that saw a decline in property prices were Auckland (down 8.3% year-on-year) and Wellington (down 9.3%), with prices in Wellington City alone losing 21.8%. On the opposite end of the spectrum, house prices in the West Coast were up 25% – by far the greatest regional percentage increase in August.

It’s a further confirmation that, since its peak in November 2021, the property market has changed significantly, opening up new opportunities for buyers. Will sales activity pick up speed in the warmer months?

Source: REINZ Monthly Property Report, August 2022

More buyers attending open homes

According to REINZ chief executive Jen Baird, sales activity remains subdued despite property prices easing, with rising mortgage rates and concerns around inflation putting the brakes on the market.

“That said, some real estate agents are reporting an increase in open home attendance,” said Baird. “And while owner-occupiers remain a dominant force in the market, first-home buyers are beginning to re-emerge.”

On the one hand, as REINZ reports, vendors are adjusting their price expectations; on the other, CCCFA rules have recently been eased and more changes have been announced – making property more attractive for buyers.

What are economists saying?

As housing market trends continue to show us time and again, predicting short-term price movements is very intricate and unlikely. Nonetheless, it’s still interesting to read what economists are saying in the current environment.

For example, according to independent economist Tony Alexander, the housing market is at a turning point. In the past few weeks, Alexanders’ surveys of mortgage advisers and real estate agents found that first-home buyers are moving back into the market, looking to take advantage of easing prices and increasing supply.

“Spring for 2022 looks like being one in which housing as an asset to grow one’s family in [as opposed to an investment asset] becomes dominant,” Alexander said. “What will follow is the flow of people who treat housing as a portfolio asset, and that is when price movement can surprise.”

ASB economist Nathaniel Keall was not of the same mind: “The usual activity metrics we look to for a signal on the direction of travel were looking mixed this month, meaning there’s no clear smoking gun for signs the market may be on the turn.”

Other economists, like ANZ’s economic team, believe there is still some way to go before property market activity regains steam. And a lot will come down to inflation and mortgage rates.

Kiwibank’s senior economist Jeremy Couchman tried to put things into perspective. “We are forecasting house prices to be 13 per cent lower by year end. A dramatic fall for sure. But a 13 per cent trough would only take the House Price Index back to levels seen at the start of 2021,” Couchman said. “From early next year, we see a gradual recovery in prices. Gradual because significant new housing supply is far outstripping new housing demand.”

Like to talk?

If your fixed-term mortgage rate is due to expire soon, or need a mortgage for your next property move, please don’t hesitate to contact us. While we don’t know what the future may hold, we can help you understand your options and structure your home loan based on your needs.

Disclaimer: Please note that the content provided in this article is intended as an overview and as general information only. While care is taken to ensure accuracy and reliability, the information provided is subject to continuous change and may not reflect current developments or address your situation. Before making any decisions based on the information provided in this article, please use your discretion and seek independent guidance.